BLOG DEL BANCO SANTANDER

![]()

Understanding payslips: a guide on how to read your payslip

SAVINGS AND INVESTMENT I March 24, 2021

Web Content Viewer

Actions

Web Content Viewer

Actions

BLOG DEL BANCO SANTANDER

![]()

SAVINGS AND INVESTMENT I March 24, 2021

Web Content Viewer

Actions

Web Content Viewer

Actions

*Post updated in January 2024

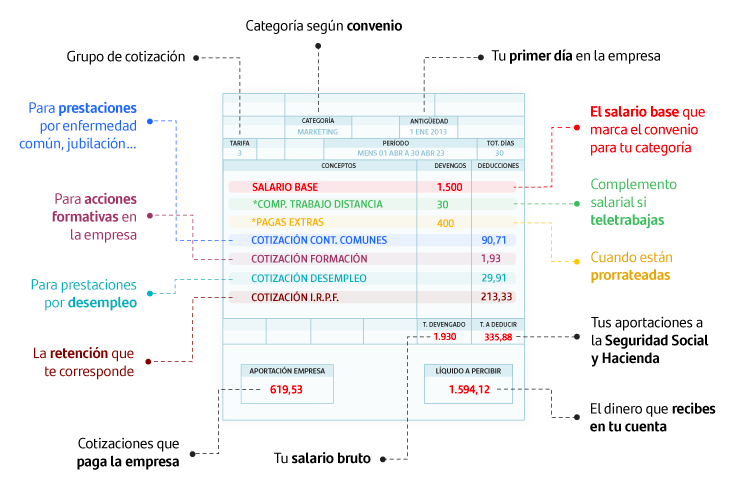

Even though payslips are important in our lives, you have probably had some doubts on more than one occasion when you have taken time to really look at them properly, because you were not sure about what some of the items on them are. So that you no longer have to worry about this, we have put together a useful guide on how to read and understand your payslip in 2024: it explains what this document is about and all of the key information within it.

A payslip is a document that the company has to give each employee by law. It contains a range of details about the company, the type of work that you have done, the time worked, and different financial amounts. It is a receipt for payment of your salary, and also proof that you have paid your social security contribution, as an employee, and of the amount of tax withheld as part of your income tax payment (IRPF). In addition, as it has been filled out and signed by the company, the document has legal force should there be any problems relating to it.

The payslip acts as evidence of social security payments made and personal income tax (IRPF) withholdings, but also as a receipt of payment, and as such it must contain information concerning the type of work done, and the amounts received for a number of items.

The company must provide basic information about its business activity, such as:

It must also contain the employee's basic information:

These data refer to the relationship between the employer and the employee. This is considered to be the basic information that must appear on a payslip, though more specifications may be added.

Below, we will give you an overview of the different sections of a payslip, and the information that must appear in each of them.

The basic sections of a payslip in 2024 are:

Each of these sections will contain different information, which you must be familiar with in order to read and understand this document properly.

Under regulations, some data, which identify the company and you as an employee to the Spanish Public Employment Service (SEPE), Social Security and the Tax Authority, must be included in the payslip. What information must appear in the header of a payslip?

The company section will include:

The following will be shown in the employee section:

The payment period must also appear in this section.

These data may also be supplemented with other details, such as the collective agreement that applies to the employee, the employee's current account, and other data.

Accruals are the earnings you receive for the services that you have performed during the month corresponding to the payslip. They are your total gross remuneration and are divided into two categories.

Salary-related payments or accruals are the amounts paid to you as remuneration for your work. There are normally several breakdowns, which, when totalled, is known as the gross salary. These breakdowns contain the following:

These are goods and services that you receive from the company, which are not treated as taxable pay. They are not liable for any IRPF deductions, and some of them are also exempt from social security payments.

The following are considered non-salary accruals:

Deductions from a payslip include payments by the employer to social security to cover any absences due to incapacity, your future pension or your unemployment benefit, which are deducted from your income. A withholding will also be deducted as an advance on income tax, which will be finalised when you submit your tax return. The main deductions that you will see on your payslip are:

These social security contributions by the employee include:

This is an advance on what you will have to pay in your tax return, which will specify the exact sum. The percentage of this withholding is not fixed, as it will depend on what you earn (it is a progressive tax), and on your personal and family circumstances (such as your marital status, number of children, dependent persons and level of disability). The minimum withholding is 2%, but this may be adjusted. The average is around 15%. Modelo 145, which you fill out when you begin working or when your circumstances change, will determine the percentage of personal income tax that will be withheld from your payslip.

You are entitled to advance payments for work that you have already done before pay day. In this case, the deduction for the money requested will be included in this section.

This value is the assessed value any of products in kind, which are already included in the accruals section as "Payment in kind".

Union dues may be included here, if applicable.

Once you know how much the accruals and deductions add up to, you will finally know how much the company is going to pay into your account. The net amount to be received is your net salary, i.e. what you are actually going to get. It is calculated by subtracting the deductions amount from the total accruals.

The lower section of your payslip must also contain a box with the signature and/or stamp of the company, the payer, with the date of delivery for the payslip and a space for "receipt", where employees must sign and state the date on which they received their pay (if the company keeps a copy). Optionally, the number of the account where the salary is paid in may also appear here.

The usual procedure is for special payments to accrue annually or twice a year. The extra payments are generated from the day on which the previous one is paid, i.e. if they are accrued annually, the extra Christmas payment is generated for the period worked between 1 January and 31 December of the corresponding year, and if it is accrued twice a year, for the period worked between 1 July and 31 December.

The extra payments may be paid in the corresponding months or on a pro rata basis, i.e. spread over the twelve monthly payments. The collective agreement determines how these amounts are paid.

Irrespective of whether they are paid on a pro rata basis, the employee pays social security contributions for the extra payments in their payslip each month. This is set out in the common contingencies section of your payslip.

If they are not paid on a pro rata basis, only the percentage corresponding to personal income tax will be withheld in the month in which the extra payment is paid (normally June or July, and December), as the social security contributions have already been paid every month.

What happens if the company does not give you your payslip? As established in Article 29 of the Spanish Workers' Statute, salaries must be calculated and paid on time, and with documented evidence thereof, in the place and on the date agreed and "the salary will be documented by giving the employee an individual slip as proof of payment of thereof". This payslip can be delivered on paper or via email. Therefore, sanctions may be imposed for failure to provide a payslip or failure to do so correctly. The Spanish Law on Labour Infringements and Sanctions stipulates that:

If, when you have submitted a claim, you do not receive a payslip, you may go through the legal system to request payslips in writing.

Are you more familiar with your payslip now? Do you know what information it contains and why you must keep it for any claims or requests? Check that the proper deductions have been made, and compare the gross annual salary to check whether it has changed.

If you want a salary account which your income can be paid into, take a look at the different current account options at Banco Santander. If you want, you can also current account options at Banco Santander. If you want, you can also calculate your net salary with our calculator.

Web Content Viewer

Actions

Rate this item

Tu valoración ha sido guardada.

Web Content Viewer

Actions

Related posts