BLOG DEL BANCO SANTANDER

![]()

Everything you need to know about the modelo 145 form

PYMES Y NEGOCIOS I January 27, 2021

Web Content Viewer

Actions

Web Content Viewer

Actions

BLOG DEL BANCO SANTANDER

![]()

PYMES Y NEGOCIOS I January 27, 2021

Web Content Viewer

Actions

Web Content Viewer

Actions

The modelo 145 form is a Tax Agency form dedicated to personal income tax (IRPF) through which taxpayers inform their payer (normally, their employer) about their tax and family status, which is then used to define the income tax withholding percentage applied to their wages.

This document is essential to your income tax return for the year, which you will file the following year, as it will serve as the basis for calculating the personal income tax withholding applied to your wages each month. Therefore, just how accurately you fill in the modelo 145 form will have a significant impact on your net salary.

The tax authority obliges your payer, i.e. the company you work for, to withhold a portion of your income as tax payable subsequently on your income tax return. In this sense, your family circumstances (if you have dependants or you are considered a large family by Spanish law) and personal circumstances (for example, if you have a disability), will have an influence on the calculation of your withholding percentage.

Usually, you are asked to fill in the modelo 145 form when you start working for a company, or when there is a change in the personal or family circumstances you had reported previously. In fact, this information must be provided before the first day of the year or the start of the contractual relationship with the company, indicating your personal and family circumstances at that time.

However, as many employees forget to inform their employer of these changes, or they are unaware that they are required to or are not sure how to do so, many companies will ask their employees to fill the form in at the end of the year, to identify any changes that may have occurred and that may result in a change to the IRPF withholding applied to their wages.

If there are no changes in family or personal circumstances, there is no need to repeatedly provide the payer with these details.

If your personal and family circumstances change having submitted the modelo 145 form, and these entail a reduction in your withholding percentage, for example, the birth of a child, you can file a new form. The changes will take effect from the date of communication, provided that there are at least five days until the next payroll date.

If there is a change in your personal or family circumstances that involves a higher withholding percentage being applied, you must report this to your company within 10 calendar days of the date of the change. The new IRPF withholding percentage will be applied to your next wage, provided that there are at least five days until the next payroll date.

If you prefer not to report any of the circumstances requested in the modelo 145 form to your employer, the IRPF withholding percentage applied by your company may be the higher than the percentage you are entitled to. In this case, when filing your tax return for the year, if more money has been withheld from your wages than should have been, you may be able to recover the difference.

Furthermore, bear in mind that a tax infringement is constituted by the inclusion of false, incomplete or inaccurate data in the modelo 145 form, or by failure to report changes in your personal or family circumstances that your employer should be made aware of which, had they been known to the payer, would have determined a larger withholding. This infringement is punishable with a fine of between 35% and 150% of any amounts that have not been withheld for this reason.

Remember that if any incorrect information is included in the modelo 145 form it is you that is held responsible and not your company, which is only required to calculate the withholding percentage to be applied to your pay on the basis of any information you may have supplied.

The modelo 145 form has seven sections requesting information on your personal and family circumstances. Below we explain to you how to deal with the sections, and the data requested.

The first section concerns your personal data, i.e. you must supply your name, surnames, date of birth and identity document. You must also provide information on the following:

Fill in this section with the corresponding details if you have children or other descendants (for example, grandchildren), aged under 25 or who are disabled, regardless of their age, who live with you and whose income does not exceed €8,000 per year.

If these descendants live only with you and there is no shared custody agreement, i.e. in the case of single-parent families, select "Cómputo por entero de hijos o descendientes".

Whether you have any ascendants (parents, grandparents) dependent on you who are aged over 65 and whose annual income does not exceed EUR 8,000. Ascendants with some form of disability who reside with you should also be included here, regardless of whether they are aged 65 and over.

If you have to pay a food allowance to your children or maintenance to your partner, you should indicate this in this section, provided that these sums have been defined by a court ruling.

Select this box in the modelo 145 form if you are required to make payments for the purchase or renovation of your habitual residence using external financing, i.e. via a mortgage. You should only fill in this section if you purchased the property before 2013 and earn less than €33,007.20.

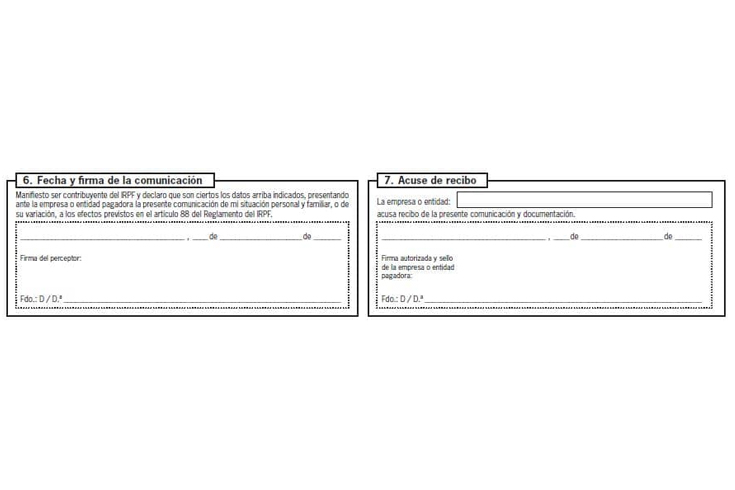

The final two sections simply provide a space for the company and the employee to sign. There is an acknowledgement of receipt which must be signed by your employer, to confirm that the withholdings are being made as per the data supplied on the modelo 145 form.

The modelo 145 form is not filed before the Tax Agency, rather it is submitted to your company or employer. The company must keep a copy on record in case the Tax Agency asks for it.

If you are self-employed, you can find information on specific financial solutions from Banco Santander for the self-employed.

Web Content Viewer

Actions

Rate this item

Tu valoración ha sido guardada.

Web Content Viewer

Actions

Related posts